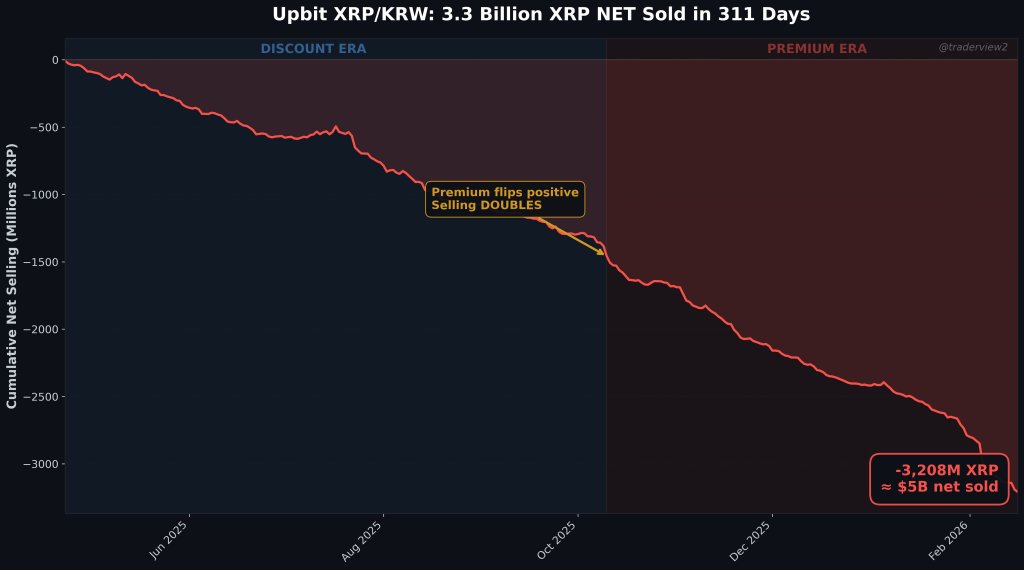

Crypto market researcher Dom (@traderview2) says he’s identified what looks like a persistent, algorithmic XRP seller on South Korea’s Upbit: one that, by his estimates, has offloaded roughly 3.3 billion XRP into the XRP/KRW order book over the past 10 months. If the analysis holds, it reframes Upbit’s XRP flow as a venue-specific phenomenon rather than a simple reflection of global risk-on/risk-off sentiment.

XRP/KRW Saw $5 Billion in Net Selling

Dom analyzed “82 million trades on Upbit XRP/KRW” and mapped their net imbalance over time. His headline conclusion: “A $5 billion one directional selling pipeline running 24/7 for almost a year.”

Dom said the work began after an intense intraday stretch that forced a closer look at the tape. “It started with yesterday’s price action. -57M XRP in CVD over 17 hours. It looked insane,” he wrote. “So I ran forensic queries – bot fingerprinting, iceberg detection, wash trade checks. The selling was real. Algorithmic. 61% of trades fired within 10ms. Single bot running 17 hours straight with one 33 second pause.”

Instead of treating that -57 million XRP cumulative volume delta as an outlier, Dom said he zoomed out and found it matched a longer-running pattern. “-57M isn’t an anomaly,” he wrote. “Upbit XRP/KRW has been net negative every single month for 10 months,” listing several months with large net selling: “Apr: -165M,” “Jul: -197M,” “Oct: -382M,” and “Jan: -370M.” In total, he put the figure at “3.3 BILLION XRP in net selling. ~$5B.”

He also argued the flow is unusually consistent. “Only 1 week out of 46 was positive. One,” Dom wrote, adding that there is “no weekday/weekend distinction” and “no time of day where buying outweighs selling in aggregate.” That persistence is part of why he framed it as something closer to execution infrastructure than discretionary trading. “This isn’t a trader,” he wrote. “It’s infrastructure.”

A key part of the thread is the cross-venue comparison. Dom said Binance’s XRP/USDT market showed materially less sell pressure during the same windows—“2-5x less sell pressure on the same coin,” he wrote, pointing to a June period where “Binance was net positive while Upbit bled -218M.”

He also flagged a weak relationship between the two venues’ hour-by-hour flow, claiming “the hourly correlation between the two venues is only 0.37,” which would imply Upbit’s net selling is being driven by local factors rather than simply mirroring global positioning.

XRP Traded Cheaper In Korea For Months

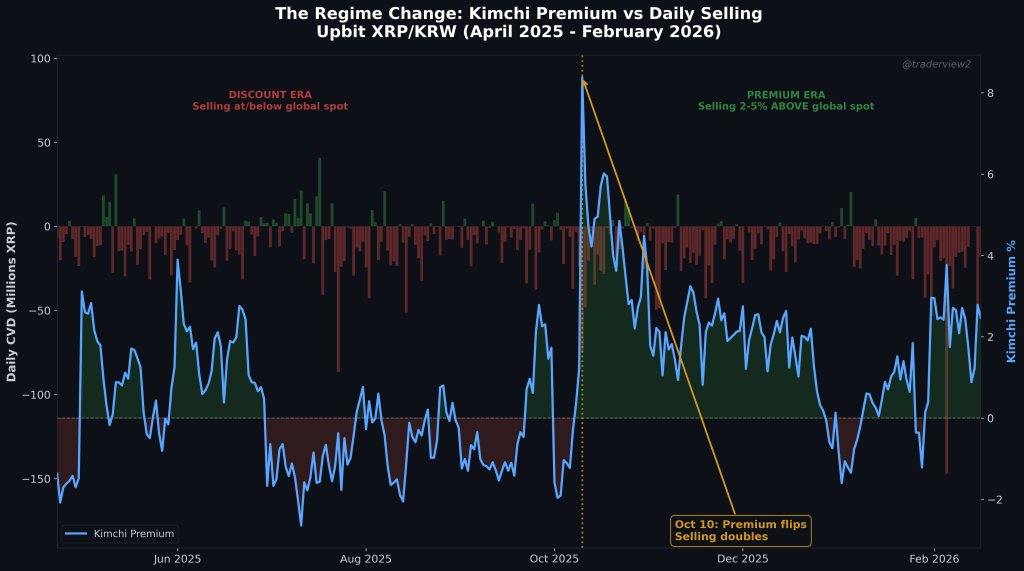

Dom’s pricing observations added another layer. He said that from April through September, Upbit XRP traded “3-6% BELOW Binance,” calling it a “reverse Kimchi discount.” In his view, that detail matters because it suggests the seller was willing to accept consistently worse execution than what was available elsewhere.

“The sellers were accepting 6% worse fills than available on global markets, for many months,” Dom wrote. “They don’t care about the price. They need KRW, are mandated to use Upbit, and/or are Korean holders taking profit…”

He then pointed to what he described as a structural break around Oct. 10. “Korean retail went insane. Premium flipped from -0.07% to +2.4% in a single day. Trades 5x’d to 832K,” Dom wrote, adding that the premium “has only briefly gone negative since.” The seller, in his telling, did not back off—if anything, the pace increased. “And the sellers? They doubled their daily rate. From -6.3M/day to -11.2M/day.”

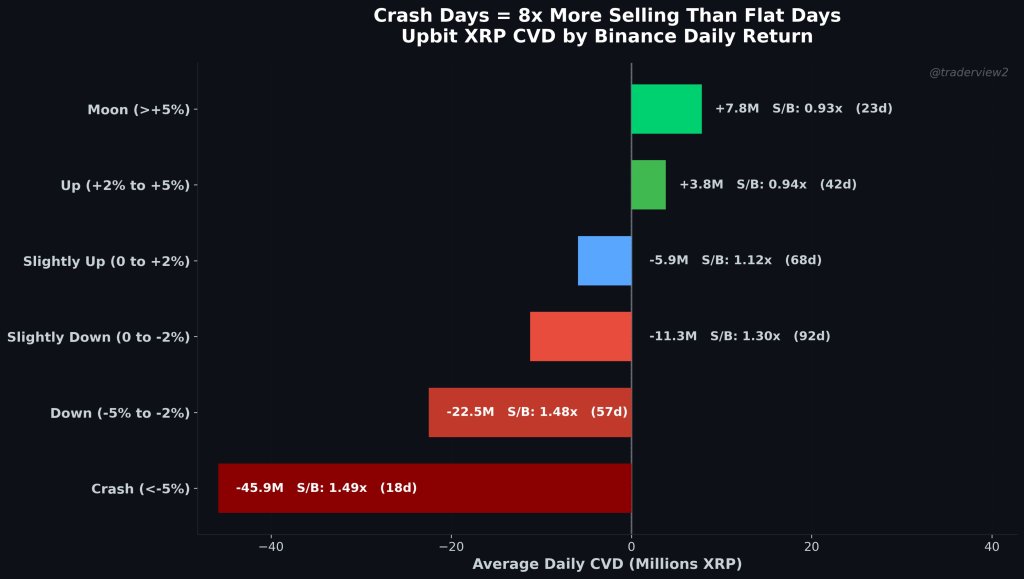

Dom tried to connect that behavior to market regimes by “bucket[ing] every day by what XRP did on Binance globally,” reporting that Upbit flow skews heavily negative on down days and especially on crash days.

He summarized the dynamic as feedback between a systematic seller and retail behavior: “On moon days, Korean retail becomes a NET BUYER. They’re accumulating,” he wrote. “On crash days, sell intensity is 8x heavier. The systematic seller + retail panic amplify each other. Korean retail buys every rip. The pipeline sells into all of it.”

To support the “machine versus retail” framing, Dom contrasted order-size fingerprints on both sides of the tape. He claimed the sell side repeatedly used round-number clips—“10, 50, 100, 500, 1000 XRP”—with “57-60% of all trades fire within 10ms,” while the buy side showed a large fraction of “tiny fractional sizes,” such as “2.535, 3.679, 2.681 XRP,” which he argued is consistent with KRW-denominated retail tickets like buying a fixed won amount of XRP. “One side looks like retail,” he wrote. “The other looks like a machine.”

The scale claim is also central to why the thread traveled. Dom said “3.3 billion XRP” represents “5.4% of XRP’s entire circulating supply,” moved through “a single trading pair, on a single exchange, in 10 months.” He emphasized he’s working from trade-level datasets: “This analysis used tick trade data I collected from Upbit and Binance,” he wrote, citing “82M Upbit trades + 444M Binance trades.”

Dom stopped short of naming a specific entity behind the selling, instead posing a question he framed as the next investigative step: who can sustain “300-400M per month for a year straight,” seemingly “doesn’t care about 6% discounts,” and “needs KRW specifically or is in some walled garden and can only use Upbit?”

At press time, XRP traded at $1.45.

English (US)

English (US)